Who Led Vape Sales in H1? RELX Leads While FLOW Surges

In 2018, the vaping boom arrived, with 18 financing deals completed in the primary market according to incomplete statistics, totaling about RMB 1 billion. Recently, EC E-Cigarette World reported that by early August 2019, more than 35 vaping brands had s

In 2018, the "windfall" of e-cigarettes arrived. According to incomplete statistics, the primary market completed 18 financing events, with a total financing amount estimated at around 1 billion yuan. Recently, according to statistics from "EC E-Cigarette World," as of early August 2019, over 35 e-cigarette brands have completed financing, with a total financing amount exceeding 1 billion yuan. Especially after May, it entered a peak period for e-cigarette brand financing!

The popularity of e-cigarettes can be seen not only from investment and financing but also reflected in the shipment volume and sales of e-cigarette brands. According to research data from Guojin Securities, the shipment volume and sales of e-cigarettes surged in the first half of 2019, especially in online channels. With the addition of e-commerce platforms like JD and Tmall, the online transaction volume of the e-cigarette industry nearly doubled in the first half of this year!

From the shipment volume and sales of major e-cigarette brands in the first half of the year, RELX leads the industry, while FLOW has surged to follow closely behind, followed by Gippro, Shanlan, IQOS, and JuuL!

In terms of sales volume, RELX has consistently ranked first in the industry in the first half of the year. Before April, Gippro held the second position, but after FLOW launched in April, it was quickly surpassed, placing Gippro in third and FLOW in second.

In the first half of the year, the online channel for e-cigarettes exploded, with both shipment volume and sales experiencing significant growth.

Data shows that the online sales of the e-cigarette industry reached 1.089 billion yuan in the first half of this year, a year-on-year increase of 90.96%. In June, influenced by the "618 Shopping Festival," sales grew by 149.41%. The e-cigarette industry has already achieved about 85% of last year's sales in just half a year, and it is expected that the overall sales of the industry will continue to grow strongly this year. In the first half of the year, the sales of devices and e-liquids accounted for 83.25% and 16.75%, respectively. Among them, the sales of devices amounted to 907 million yuan, while e-liquids and pods accounted for 183 million yuan.

Looking at the sales volume of e-cigarette brands, since the beginning of 2019, the leading brands in shipment volume are RELX, FLOW, Gippro, Shanlan, IQOS, and JuuL! RELX has consistently ranked first in sales volume in the first half of the year, while Gippro held the second position until FLOW launched in April, which then became the second, pushing Gippro to third place!

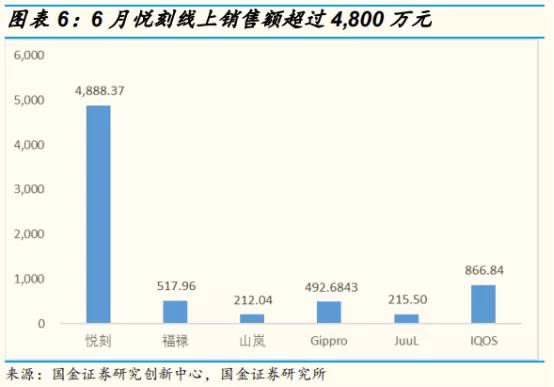

For RELX, its sales growth rate exceeded 30% in June. In the first half of the year, RELX achieved sales of 177 million yuan. In the same period, the well-known American e-cigarette brand JuuL had an online sales volume of only 5.8892 million yuan, while the heat-not-burn star brand IQOS achieved sales of 28.8347 million yuan. In June, RELX achieved sales of 48.8837 million yuan. In terms of sales volume, RELX continued to lead among the aforementioned brands, achieving a sales volume of 1.3855 million units in the first half of the year.

Monitoring data shows that the online launch times of various brands vary significantly. RELX started selling in July last year, while FLOW only began sales in April this year, thus lacking a direct comparison for the same period. However, looking at the month-on-month data, RELX's sales in June increased by 36% and 38% in terms of sales volume. IQOS also saw a 50% increase in both sales and volume.

Additionally, Shanlan has a relatively complete historical data set, showing that its sales and volume increased by 49.51% and 205.04%, respectively, in the first half of the year. This indicates that Shanlan maintained a stable growth rate in sales during the first half of the year!

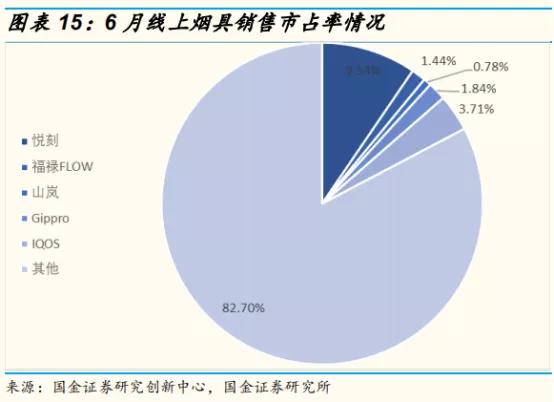

Overall, RELX's position as the leading e-cigarette brand remains solid. In June, RELX's online sales market share reached 9.54%, significantly ahead of other brands we tracked. Compared to the beginning of this year, RELX's online market share increased by 0.72%, further solidifying its position as the top brand in the industry. On the other hand, RELX's new generation device, the "RELX Alpha," has already launched, and its rapid sales growth is worth looking forward to.

#p#分页标题#e#

#p#分页标题#e#

Meanwhile, IQOS's market share has also seen a slight increase. In June, IQOS's online market share reached 3.71%, up 0.11% from the beginning of the year. Heat-not-burn tobacco pods are currently regulated as controlled products in China and are not allowed for sale. The accessibility of consumables will also boost the sales growth of device products. Therefore, the relatively high purchasing difficulty of tobacco pods has hindered IQOS's market share growth in China.

Pod sales gradually increase; e-cigarette brands' future profitability key indicators.

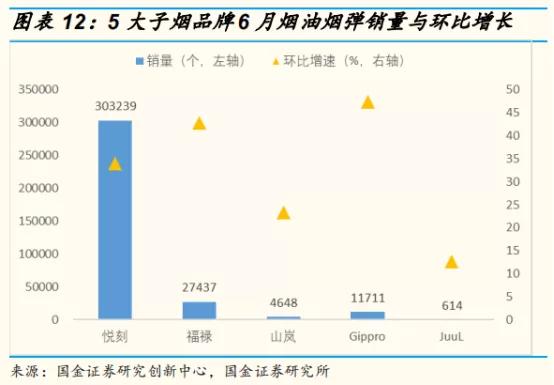

From the pod market perspective, RELX's sales of e-liquid pods exceeded 300,000 units in June. Overall, the five major e-cigarette brands saw a month-on-month increase in e-liquid pod sales in June. Among them, RELX continued its strong performance in device sales, achieving a monthly sales volume of 303,200 units, a month-on-month increase of 33.92%. RELX's cumulative sales exceeded 1 million units in the first half of the year, significantly leading other brands.

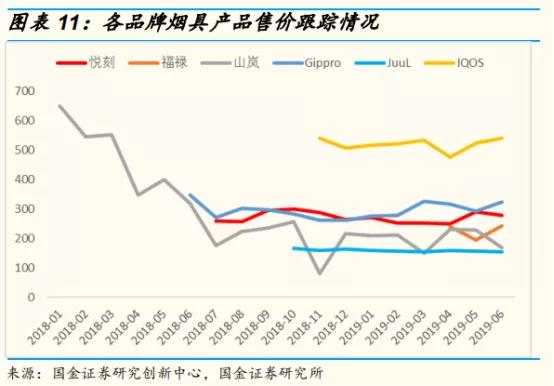

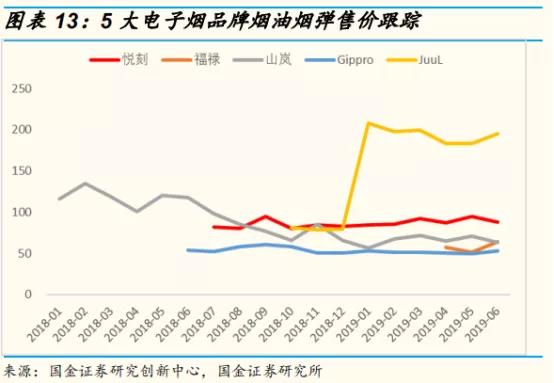

The prices of e-liquids and pods have generally seen slight increases since the beginning of the year. From historical data of various brands, except for Shanlan, which has seen a significant price drop, other brands have remained relatively stable. Entering this year, the average price of e-liquids and pods among the five major brands has remained stable, with most brands experiencing slight price increases compared to the beginning of the year. RELX's price increased by 4.69%, FLOW's by 11.01%, Shanlan's by 11.46%, Gippro's decreased slightly by 0.23%, and JuuL's decreased by 6.34%.

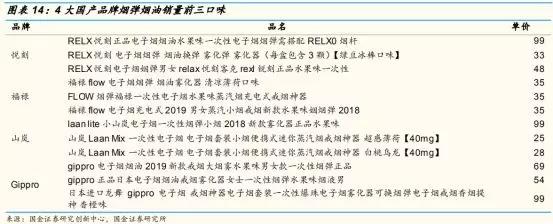

The increase in e-liquid and pod prices is related to the high sales proportion of popular products. RELX and Shanlan's popular e-liquid pods priced at 99 yuan accounted for 50% and 60% of total sales in June, respectively, indicating that the high proportion of high-priced products has contributed to the price increase. In contrast, FLOW's popular e-liquid pods are priced at only 35 yuan and account for only 5%, indicating that this brand's price increase relies on other non-popular e-liquid pods. Gippro's top-selling e-liquid pod is priced at 69 yuan, while the second-best-selling pod is priced at 54 yuan, with only a slight difference in sales of 84 units. However, Gippro's 99 yuan high-priced e-liquid pod accounted for only 3.94% of total sales, thus slightly suppressing the price increase.

RELX's e-liquid pod online market share reached 55.28%. RELX continued its strong performance in e-liquid pod sales, achieving an online market share of 55.28% in June, significantly increasing by 12.44 percentage points compared to the beginning of the year. Guojin Securities believes that RELX's impressive performance in e-liquid pod sales is mainly due to its continuous innovation in flavors.

Cigarette consumers tend to have high brand loyalty; once they accept a specific brand's flavor, they are likely to remain loyal to that brand for years or even decades. However, e-cigarette consumers tend to have lower loyalty to brands, with flavor being the primary motivation for purchases.

From the sales structure of various brands, the sales proportion of e-liquids and pods has been on the rise. Among them, RELX's e-liquid pod sales surpassed device sales in February this year, becoming the main contributor to the brand's sales revenue. Guojin Securities believes that the contribution of e-liquids and pods to brand sales revenue depends on the number of flavors available.

RELX offers 15 flavors of pods, with its pod revenue accounting for 54.67%, while Gippro only has 5 flavors, with pod revenue accounting for 12.53%. The sales elasticity of e-liquids and pods is greater than that of devices. Looking at the month-on-month growth of the four major domestic brands' devices and e-liquids and pods, the sales growth of e-liquids and pods significantly outpaces that of devices. As consumables, e-liquids and pods inherently have better growth potential, and with the introduction of various innovative e-liquid flavors, the future market scale is expected to catch up with that of devices. For instance, Hike has launched a business model allowing consumers to purchase devices for just 1 yuan!

The popularity of e-cigarettes can be seen not only from investment and financing but also reflected in the shipment volume and sales of e-cigarette brands. According to research data from Guojin Securities, the shipment volume and sales of e-cigarettes surged in the first half of 2019, especially in online channels. With the addition of e-commerce platforms like JD and Tmall, the online transaction volume of the e-cigarette industry nearly doubled in the first half of this year!

From the shipment volume and sales of major e-cigarette brands in the first half of the year, RELX leads the industry, while FLOW has surged to follow closely behind, followed by Gippro, Shanlan, IQOS, and JuuL!

In terms of sales volume, RELX has consistently ranked first in the industry in the first half of the year. Before April, Gippro held the second position, but after FLOW launched in April, it was quickly surpassed, placing Gippro in third and FLOW in second.

In the first half of the year, the online channel for e-cigarettes exploded, with both shipment volume and sales experiencing significant growth.

Data shows that the online sales of the e-cigarette industry reached 1.089 billion yuan in the first half of this year, a year-on-year increase of 90.96%. In June, influenced by the "618 Shopping Festival," sales grew by 149.41%. The e-cigarette industry has already achieved about 85% of last year's sales in just half a year, and it is expected that the overall sales of the industry will continue to grow strongly this year. In the first half of the year, the sales of devices and e-liquids accounted for 83.25% and 16.75%, respectively. Among them, the sales of devices amounted to 907 million yuan, while e-liquids and pods accounted for 183 million yuan.

Looking at the sales volume of e-cigarette brands, since the beginning of 2019, the leading brands in shipment volume are RELX, FLOW, Gippro, Shanlan, IQOS, and JuuL! RELX has consistently ranked first in sales volume in the first half of the year, while Gippro held the second position until FLOW launched in April, which then became the second, pushing Gippro to third place!

For RELX, its sales growth rate exceeded 30% in June. In the first half of the year, RELX achieved sales of 177 million yuan. In the same period, the well-known American e-cigarette brand JuuL had an online sales volume of only 5.8892 million yuan, while the heat-not-burn star brand IQOS achieved sales of 28.8347 million yuan. In June, RELX achieved sales of 48.8837 million yuan. In terms of sales volume, RELX continued to lead among the aforementioned brands, achieving a sales volume of 1.3855 million units in the first half of the year.

Monitoring data shows that the online launch times of various brands vary significantly. RELX started selling in July last year, while FLOW only began sales in April this year, thus lacking a direct comparison for the same period. However, looking at the month-on-month data, RELX's sales in June increased by 36% and 38% in terms of sales volume. IQOS also saw a 50% increase in both sales and volume.

Additionally, Shanlan has a relatively complete historical data set, showing that its sales and volume increased by 49.51% and 205.04%, respectively, in the first half of the year. This indicates that Shanlan maintained a stable growth rate in sales during the first half of the year!

Overall, RELX's position as the leading e-cigarette brand remains solid. In June, RELX's online sales market share reached 9.54%, significantly ahead of other brands we tracked. Compared to the beginning of this year, RELX's online market share increased by 0.72%, further solidifying its position as the top brand in the industry. On the other hand, RELX's new generation device, the "RELX Alpha," has already launched, and its rapid sales growth is worth looking forward to.

#p#分页标题#e#Meanwhile, IQOS's market share has also seen a slight increase. In June, IQOS's online market share reached 3.71%, up 0.11% from the beginning of the year. Heat-not-burn tobacco pods are currently regulated as controlled products in China and are not allowed for sale. The accessibility of consumables will also boost the sales growth of device products. Therefore, the relatively high purchasing difficulty of tobacco pods has hindered IQOS's market share growth in China.

Pod sales gradually increase; e-cigarette brands' future profitability key indicators.

From the pod market perspective, RELX's sales of e-liquid pods exceeded 300,000 units in June. Overall, the five major e-cigarette brands saw a month-on-month increase in e-liquid pod sales in June. Among them, RELX continued its strong performance in device sales, achieving a monthly sales volume of 303,200 units, a month-on-month increase of 33.92%. RELX's cumulative sales exceeded 1 million units in the first half of the year, significantly leading other brands.

The prices of e-liquids and pods have generally seen slight increases since the beginning of the year. From historical data of various brands, except for Shanlan, which has seen a significant price drop, other brands have remained relatively stable. Entering this year, the average price of e-liquids and pods among the five major brands has remained stable, with most brands experiencing slight price increases compared to the beginning of the year. RELX's price increased by 4.69%, FLOW's by 11.01%, Shanlan's by 11.46%, Gippro's decreased slightly by 0.23%, and JuuL's decreased by 6.34%.

The increase in e-liquid and pod prices is related to the high sales proportion of popular products. RELX and Shanlan's popular e-liquid pods priced at 99 yuan accounted for 50% and 60% of total sales in June, respectively, indicating that the high proportion of high-priced products has contributed to the price increase. In contrast, FLOW's popular e-liquid pods are priced at only 35 yuan and account for only 5%, indicating that this brand's price increase relies on other non-popular e-liquid pods. Gippro's top-selling e-liquid pod is priced at 69 yuan, while the second-best-selling pod is priced at 54 yuan, with only a slight difference in sales of 84 units. However, Gippro's 99 yuan high-priced e-liquid pod accounted for only 3.94% of total sales, thus slightly suppressing the price increase.

RELX's e-liquid pod online market share reached 55.28%. RELX continued its strong performance in e-liquid pod sales, achieving an online market share of 55.28% in June, significantly increasing by 12.44 percentage points compared to the beginning of the year. Guojin Securities believes that RELX's impressive performance in e-liquid pod sales is mainly due to its continuous innovation in flavors.

Cigarette consumers tend to have high brand loyalty; once they accept a specific brand's flavor, they are likely to remain loyal to that brand for years or even decades. However, e-cigarette consumers tend to have lower loyalty to brands, with flavor being the primary motivation for purchases.

From the sales structure of various brands, the sales proportion of e-liquids and pods has been on the rise. Among them, RELX's e-liquid pod sales surpassed device sales in February this year, becoming the main contributor to the brand's sales revenue. Guojin Securities believes that the contribution of e-liquids and pods to brand sales revenue depends on the number of flavors available.

RELX offers 15 flavors of pods, with its pod revenue accounting for 54.67%, while Gippro only has 5 flavors, with pod revenue accounting for 12.53%. The sales elasticity of e-liquids and pods is greater than that of devices. Looking at the month-on-month growth of the four major domestic brands' devices and e-liquids and pods, the sales growth of e-liquids and pods significantly outpaces that of devices. As consumables, e-liquids and pods inherently have better growth potential, and with the introduction of various innovative e-liquid flavors, the future market scale is expected to catch up with that of devices. For instance, Hike has launched a business model allowing consumers to purchase devices for just 1 yuan!

Related Articles

Vaping News

Ahead of a Nationwide Ban, Hundreds of Russian Retailers Voluntarily Stop Selling Vapes

2026-04-16

Vaping News

Illegal Vape Brands Try to Evade FDA Scrutiny by Posing as “Made in the USA”

2026-04-08

Vaping News

Jordan’s New Tobacco Control Rules: Waterpipe Tobacco Market Set for Major Changes

2026-03-17