Analysis of Offline Sales Models for Domestic E-Cigarette Brands

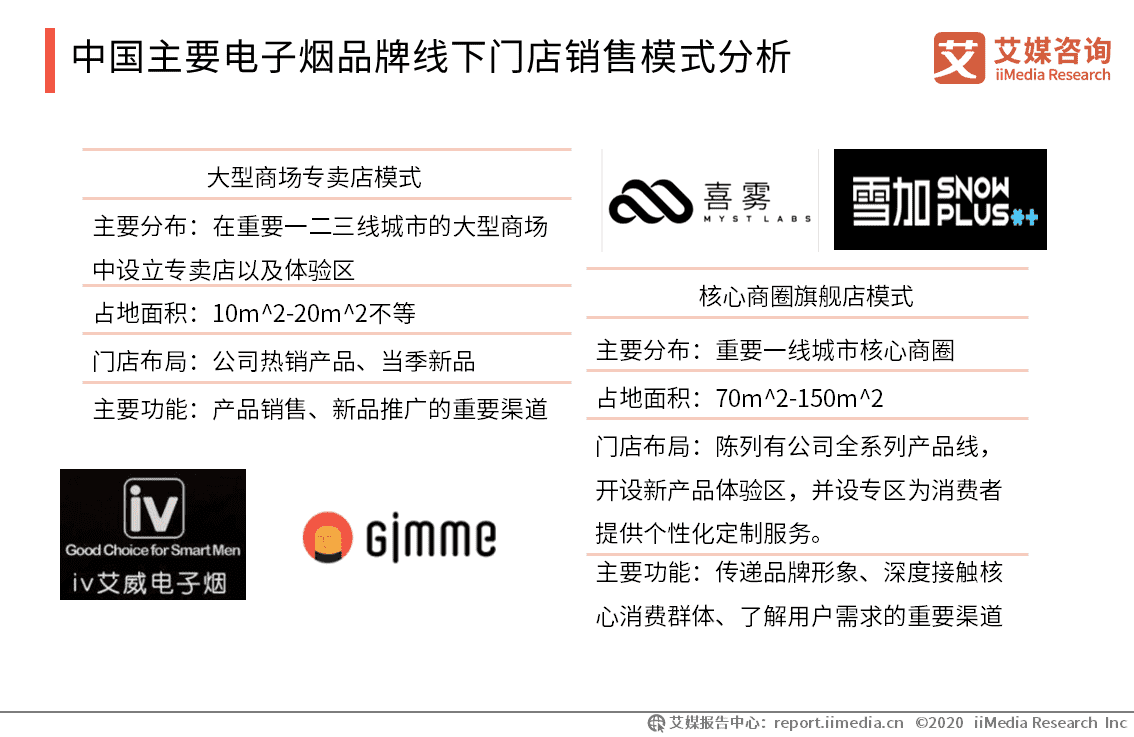

Analysis of Offline Store Sales Models of Major Chinese Vaping Brands

As relevant policies have been introduced and controls on online vaping sales have become increasingly strict, major vaping brands have shifted toward offline expansion to capture market share. Their offline store operating models have also become more diverse. In addition to traditional offline channels such as convenience stores, 3C retail franchise stores, and distributor-operated stores, newer offline channels have also emerged, including mall specialty stores and flagship stores in prime commercial districts.

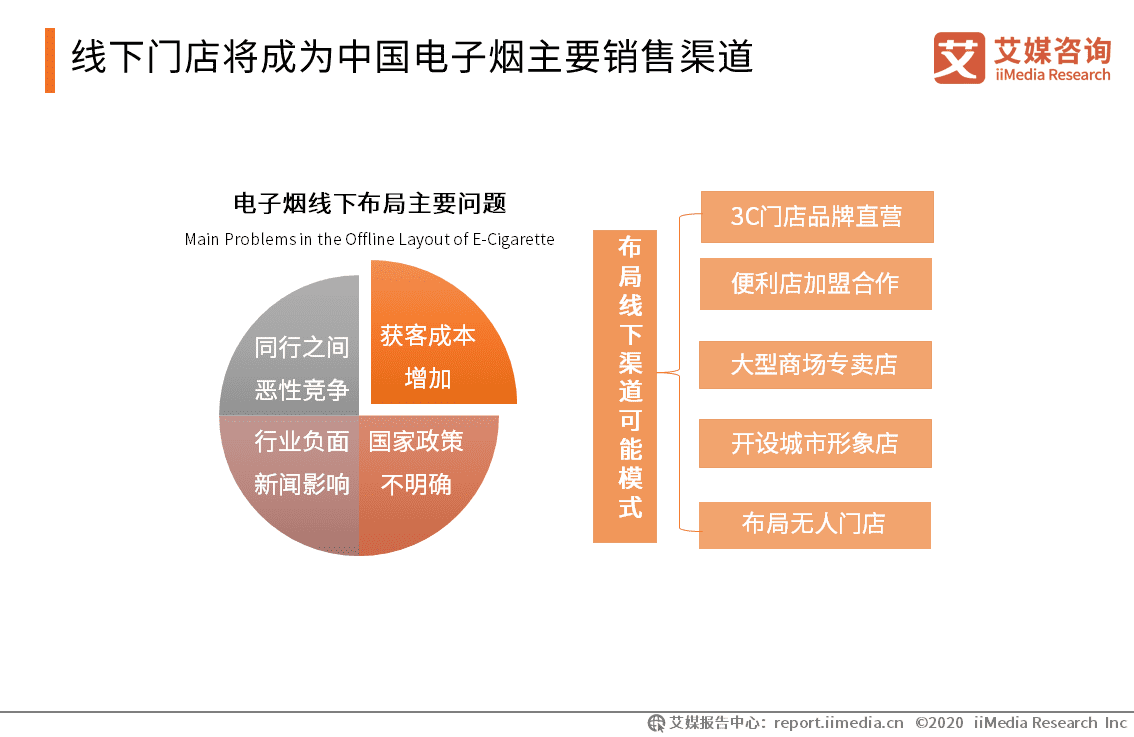

Offline stores will become the main sales channel for vaping products in China

With the introduction of national policies banning online sales, online sales channels for vaping products have been blocked, and a number of weaker small and medium-sized enterprises have exited the market, pushing the industry into a reshuffling phase. Facing severe survival pressure, vaping brands have all turned to offline expansion. Analysts at iiMedia Research believe that because the total resources available to offline merchants and stores are limited, vaping brands will compete aggressively for channel resources, meaning the shift to offline channels will bring even fiercer competition.

iiMedia Research analysts also believe that compared with online channels, offline channels require greater investment. At present, the main models are brand-operated stores and franchise partnership models, and vaping brands can choose according to their financial strength. In the future, as national regulatory policies gradually stabilize, companies can achieve more precise marketing by building centralized data platforms, and can also deploy unmanned stores to reduce offline sales costs.