E-cigarettes are entering a major offline growth phase: who can secure a good location and good prod

This article is transferred from Blue Hole New Consumption

At the end of 2020, on the opening day of Wuhan's first Chayan Yuese Milk Tea Shop, the cold weather in early winter did not cool down the popularity of this new store. On the contrary, many people were already waiting at the store in the early morning of the previous day.

Under a winding long line, the customers at the end of the line will have to wait about 8 hours to get their cup of tea Yanyue, and this time is enough for them to make two round-trips from Wuhan to Changsha (the birthplace of tea Yanyue).

Fried shoes, fried blind boxes, and fried handmade products. Under the extreme imbalance between supply and demand, even milk tea can be hyped. A cup of milk tea sells for between 15 and 20 yuan. In the hands of scalpers, the price of one cup even reaches 500 yuan.

The consumption habits of the new generation seem to have never been understood by the public, but their ability to attract money and purchasing power are pushing one company after another to enter the spotlight of the capital market.

Station B, Xicha, Bubble Mart, Haidilao, and Xiaoxiong Electric have created new consumption scenarios through new consumption types in one traditional consumer industry after another, led by new consumption concepts.

When new consumption concepts and scenarios collided with tobacco, e-cigarettes were born. After experiencing barbaric growth and strong online supervision, the concept of e-cigarettes has been swaying between tuyere and pseudo-tuyere.

In 2020, a sudden epidemic swept across the country, and the offline retail industry suffered a major blow. As shop owners who do beauty, manicure, and catering switch to physical e-cigarette shops that "return money quickly and make more profits", e-cigarettes, this once-forgotten industry, have once again returned to the public's attention.

01 The secondary wind comes

According to statistics from the World Health Organization, among the world's 7.5 billion people, the number of smokers has reached 1 billion.

Among them, the number of smokers in China ranks first in the world with 287 million, surpassing the total number of smokers in other top ten countries combined.

At the same time, in terms of consumption, China's cigarette consumption accounts for 44% of the global total, which is a trillion-dollar market.

The emergence of e-cigarettes has stirred up this already stable Red Sea market, and the wide market space of the track is enough to breed the next super unicorn, because for now, the penetration rate of e-cigarettes in China has only reached 1.2%.

From the Red Sea market to the Blue Sea market, there is a trillion-scale growth space. Such industry growth and development expectations are enough to become capital's expectations for expected hype. This is the initial logic of industry development.

E-cigarettes themselves are not a high-threshold industry. The related technology and production of the core component-atomizers have long been mastered and conquered by China companies.

In the Shajing area of Shenzhen, China, there is a complete industrial chain. On this assembly line, 95% of the world's e-cigarettes are delivered.

At that time, there was a saying that an e-cigarette brand could be created for 5 million yuan. By negotiating orders with upstream manufacturers and labeling their own brands, e-cigarettes could enter the market as an "electronic product."

So capital launched an investment spree in the e-cigarette industry, and new brands emerged one after another. This was called the Thousand Cigarettes War at the time.

Among these new brands, we can also see star venture capitalists such as IDG, Source Capital, Sequoia Capital China, Zhenge Fund, and Shanhang Capital.

The good times did not last long. The war had just begun, and the regulatory policy had already been implemented.

In November 2019, regulatory documents were issued to completely ban online sales of e-cigarettes. Under the double blow of regulatory red lines and market competition, thousands of e-cigarette manufacturers closed down.

And this also announced that the first wave of expected e-cigarette hype came to an end.

After online blocking, offline channels have become the main battlefield for e-cigarette competition. As a new species, e-cigarettes need time to popularize and train consumers.# p#pagination title #e#

The popularity of products is the significance of offline physical stores. While online and offline channels broke out, this popularity promoted the rapid outbreak of demand. Following the epidemic, physical operators 'sentiment of "continuing to turn the tables" broke out, and the entire industry hit a high point again.

With the heavy investment of offline stores, is e-cigarettes still a good business to make money?

It can be seen from the information of a leading brand and the data of JUUL, the leading e-cigarette leader in the United States, that e-cigarettes are still a profiteering industry.

The ex-factory price of a set of e-cigarette rods priced at 299 is only 70 yuan. Although the retail terminal has received a large share of profits, the brand's gross profit margin has been maintained at around 40% in the past three years, while JUUL's gross profit margin can reach 75%.

According to an article by Aishde's Distribution Division, more than 90% of franchisees can recover the one-time input costs in the early stage within 6 months of opening. Among franchisees that have been open for more than 4 weeks, more than 60% have an average monthly net interest rate greater than 20%.

At the same time, the logic of industry development has also switched from the first stage of hype expectations to the second stage-the era of incremental competition, the competition for market share.

02 Share competition

The competition for market share lies in how to seize consumers 'needs. From this perspective, convenience and cost performance are two dimensions that remain unchanged.

Just like shared bicycles, under the premise of product homogeneity problems, one of the most important aspects of consumers 'consideration of brand selection is whether it is convenient to purchase?

High demand and fast frequency are the characteristics of e-cigarettes as consumer goods. In any scenario, once the cigarettes are exhausted, being able to purchase e-cigarettes as convenient as buying a pack of ordinary cigarettes is the core demand of consumers.

Take a leading domestic e-cigarette company as an example. It benefited from the advanced offline channel layout and quickly seized the market. Data from the brand shows that its market share in the e-cigarette industry reached 62.6%.

With the blocking of online channels, companies without financial strength or brand effect have closed down one after another, and industry resources can only be concentrated in leading companies. This is the basic law of industry development.

At present, the above-mentioned leading companies cooperate with 110 authorized distributors, owning more than 5000 specialty stores and more than 100,000 retail stores. They plan to invest a total of 600 million yuan in the next three years to develop 10000 specialty stores.

But this has not dispelled the enthusiasm of other players. On the contrary, more and more merchants are accelerating their offline layout, thereby increasing brand influence, and ultimately turning their own brands into consumers 'consumption habits.

Because what they are fighting for is not the stock market, but the incremental market for e-cigarettes to penetrate into traditional cigarettes.

The number of specialty stores currently under construction for grapefruit e-cigarettes exceeds 2500, and it is estimated that 600 million yuan will be invested this year to develop 10000 specialty stores.

Kermi plans to open 3000 specialty stores in three years, Ruwu Joy plans to open 300 stores in 2021, and reach 1000 stores in three years. ESUN Yishuang plans to build 100 benchmark stores in 2022...

This has created the current crowded situation of offline stores. With Beijing International Trade as the center, the number of offline stores of a certain brand has reached 18 within a kilometer. This situation will continue to be staged and intensified across the country in the future.

Distribution of a brand in offline stores in Beijing International Trade Area

Under such market sentiment, industry competition under the e-cigarette line has returned to the classic competition model of consumer goods: whoever can have a good position, good products, and traffic can survive in this increasingly competitive market.

03 One super and many strong, brand differentiation

The explosion of offline stores means that the industry is "involution", which will consider another dimension-whether the product is cost-effective.# p#pagination title #e#

From the current point of view, e-cigarettes have experienced price stratification. In April 2020, e-cigarette brand YOOZ released the replacement e-cigarette YOOZ Mini, with a price of 9.9 yuan; in June 2020, Hanma Group launched The "Million Set, Hundred Million Yuan Subsidy" campaign costs only 19.9 yuan per shot.

This is directly distinguished from the commonly priced cigarette bombs on the market at 39 yuan, and the cigarette rod sets that often cost more than 200 yuan. This pricing also allows these brands to harvest price-sensitive customers in the sinking market.

Price wars are not only staged among e-cigarette manufacturers, but also in online and offline channels.

Under the ubiquitous stores, consumers are more likely to buy from which distributor offers consumers the more affordable prices, which means that distributors not only have to compete with other brands, but also need to compete with the same brands. Play games between brands.

However, due to the company's agreement and supervision, they had no way to operate the pricing of goods, so they chose to tamper with gifts and engage in a disguised price war.

"Ten used cigarette bombs can come to the store to exchange them for a new cigarette bomb","Buy three boxes of cigarette bombs get one/two, or even a box","Buy a cigarette rod and get a silicone sleeve and a lanyard."

Distributors all have the idea that by surviving their nearby counterparts, they will become the final winner in this price war.

Under this kind of competition, where will the future development of the e-cigarette industry go? It is the next issue that the market pays attention to.

The price subsidy method can only gain users for a period of time, but the loyalty of such users is extremely low.

If we use the time and product power brought by burning money subsidies to seize the needs of segmented users and cultivate users 'brand loyalty, it is the breakthrough code for other brands to enter the next stage.

The attributes of consumer goods do not only lie in the goods themselves. Cultural attributes, personality labels, and added value can all meet the needs of different customers. Therefore, in the field of consumer goods, there is no exclusive monopoly.

This also explains why liquor, beer, and cigarettes are regional in the China market despite the differences in taste between different products.

The e-cigarette industry cannot break out of the general framework of consumer goods. Compared with the U.S. e-cigarette market and the traditional tobacco market, which have entered the era of stock competition, the competitive landscape of one superpower and more strong may be the answer to the next stage of market competition.

The core of competition lies not in the integration of the industrial chain or the iteration of atomizer technology, but in capturing the hearts of consumers.

Marlboro, the world's largest tobacco brand, has deeply bound it with its products through the image of a tough guy cowboy in the western United States, radiating to the world, and becoming a global leader in tobacco.

The American magazine "Capitalist" once interviewed why smokers prefer to choose Marlboro. They believe that Marlboro will bring them a sense of image superiority, which is the charm of brand culture. However, the e-cigarette industry has not yet produced a company with a unique and distinctive corporate cultural image.

At present, Marlboro accounts for 47% of the traditional tobacco market in the United States. There are still players such as Newport, Camel, and Pomay, who have occupied a place in the market through subtle differences in their own tastes and price stratification.

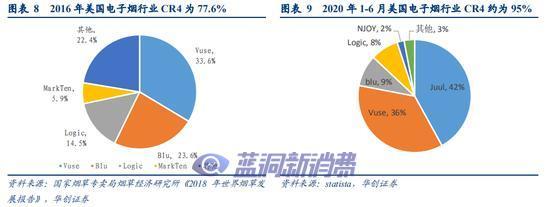

The same goes for the e-cigarette industry. Juul is the market leader, but players such as Vuse, Blu, and Logic are still closely catching up.

CR4 distribution map of the U.S. e-cigarette industry

Back in China's e-cigarette industry,"Generation Z" youth, as the main consumer force in the e-cigarette industry, have a strong enthusiasm for the pursuit of personalized taste differences.

How to customize the taste based on personality and the price stratification strategy of top players, combined with the indoctrination of brand cultural image, to create differentiated products that can bring sustainable cash flow will be the direction that e-cigarette manufacturers are striving to pursue.# p#pagination title #e#

Atomizers, tobacco oil, and all accessories are non-monopoly and do not exist in ecology. At this stage, they can be solved through outsourcing. As the scale of the industry grows larger and larger and the industry accelerates, e-cigarette manufacturers realize supply. The integration of the chain will be an inevitable result.

But until then, more importantly, they need to keep consumers firmly in their hands.