What Is Mcwell Like? Introduction to Mcwell E-Cigarette Company

What is Mcwell like? Many people may have heard of Mcwell, but not many really understand the company. Today we’ll give a detailed introduction to Mcwell’s e-cigarette business. Founded in 2009, the company mainly engages in the R&D, production, and sales

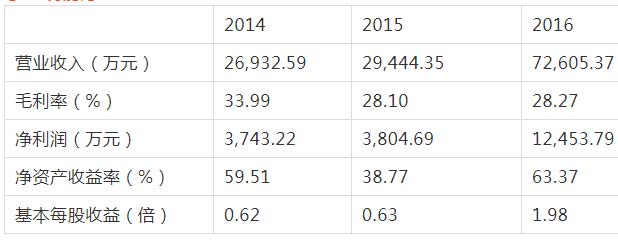

What about McWeir e-Cigarette? Many people may have heard of McWeir, but not many people really know this company. Today, Xiaobian plans to give a detailed introduction to McWeir e-Cigarette Company. The company was established in 2009. The company is mainly engaged in the research and development, production and sales of electronic cigarettes (E-cigarette) and open electronic atomization equipment APV (Advanced Personal Vaporizer). It was listed on the Third Board at the end of 2015. In 2016, the company's operating income was 726.0537 million yuan, net profit was 124.5379 million yuan, and gross profit margin was 28.27%.

The company's current business includes two major sectors: ODM and private brand APV. The company has core patented technologies for e-cigarettes such as ceramic heaters and child protection. The core team has many years of professional operation experience in R & D, manufacturing, and customer channels in the e-cigarette industry, and provides application of company patents to large overseas tobacco companies Altria, Japan Tobacco International, etc. Technology e-cigarette products. APV's own brand Vaporesso series products of the Open Electronic Atomization Equipment Division have formed a certain market scale and end customer influence in overseas markets.

The company has long-term accumulation in various aspects such as process technology, product quality, and R & D strength. The company forms the main source of income through ODM order sales and the distribution model of overseas APV atomization equipment specialty stores. During the reporting period, while ODM business increased steadily, APV business formed a stable source of income, accounting for about 30% of overall operating income.

1. company's development history

McWare Co., Ltd. was established in 2009. At the end of October and the beginning of November, the first disposable e-cigarette product reached large-scale sales. In 2012, shipments of upgraded products could reach 2 million to 3 million a month. The company's products are in the United States The market has begun to enter a rapid development cycle. In 2013, driven by customers, sales terminals in the U.S. market were established, mainly involving major pharmacies in the United States and large supermarkets such as Wal-Mart, raising the entry barrier for the industry. In 2014, it carried out capital integration with listed company Huizhou Yiwei and acquired part of the company's equity. In 2015, it obtained the national high-tech certification and was officially listed on the New Third Board. In 2016, six market-making brokerages were introduced in two rounds. In the same year, the company's technical team was established and the industry's first dust-free workshop was established. The company has a long working time and rich experience, which has promoted the establishment of industry manufacturing standards. It also helped Shenzhen Customs formulate e-cigarette export codes, making certain contributions to the development of the e-cigarette market. 2. The company's traditional ODM business and emerging APV business are driven by dual engines

2. The company's traditional ODM business and emerging APV business are driven by dual engines

The company mainly involves two parts of business, one of which is ODM business. The brand of this business belongs to customers. The company provides ODM OEM manufacturing services. The customer service is responsible for controlling the marketing, marketing, branding and distribution. Such products are mainly sold in traditional cigarette market channels, such as gas stations, convenience stores and tobacco monopoly counters in large supermarkets. They are used as a substitute for smokers to burn cigarettes in smoke-free occasions. There is no cigarette equipment in the ODM business. The other is APV's private brand business. Currently, the company has three major brands, which mainly rely on offline experience stores for sales. Traditional tobacco is like beer. To buy beer, you need to go to a supermarket. E-cigarettes are like red wine. To buy red wine, you need to go to a wine specialty store. You can get some experience and communication. The cigarette and e-cigarette markets will not overlap in the foreseeable future. In all e-cigarette offline experience stores in the United States, all APV equipment is produced by China manufacturers, but cigarette oil manufacturers are both from the United States and China.

The customers of the company's ODM business are mainly large global tobacco companies, such as Altria (Marlboro), Japan Tobacco International, British American Tobacco (35 brand cigarettes), Luxembourg, and Swedish Match. Before 2010, large tobacco companies did not intervene in the e-cigarette business, and successively entered the e-cigarette market through mergers and acquisitions of independent e-cigarette brands. For ODM business, the company only needs to do a good job in process control and quality control to meet customers 'shipment point requirements. For self-owned APV brands, in addition to products, we must also consider the issues of brand management and channel sales. In terms of private brand building, Youtube, Facebook, TWITTER and other media are used to do self-media marketing. Youtube had more than 45000 videos to promote its own brand last year, and its official website also exceeded 11 million visitors. In 2017, its own products covered 38 countries and had more than 130 agencies around the world. Overall, the company's business growth rate in the past 17 years should reach 30%. Driven by the dual engines of traditional ODM business and emerging APV business, these two aspects of business will be flat in the future.# p#pagination title #e#

3. The core technology of e-cigarettes

The four core technologies of e-cigarettes are batteries, tobacco oil, atomizer (ic), and heaters. Now, profit-making sales are the two products produced by APV and ODM. Currently, heating and non-burning tobacco is very popular on the market (accounting for 7% of Japan's traditional cigarette market, and it is expected to reach 20% this year) adopts the common platform technology of e-cigarettes, such as core heater materials, atomization technology, batteries, etc. E-cigarette technology has great extensibility. For example, medical drug delivery technology uses an electronic heater to heat a coated solid drug. The drug sublimates into a gas and is directly absorbed through the mouth. Another example is the electronic use of hookah, which does not require carbon heating. Electronic ceramic pots are used to heat hookah. Currently, such products have not yet been sold on a large scale.

4. The e-cigarette market has great room for growth

In 2016, the global market share of e-cigarettes was about US$20 billion, and the United States accounted for about 50% of the market. The United States formed large-scale sales in about 2010, which is basically the same as the time when the company formed large-scale sales. The company caught up with the U.S. market. The first step to take off. At present, the growth rate of the e-cigarette market is slowing down, not as fast as in the first five years. In recent years, the market growth rate has remained at around 17%. By 2020, the e-cigarette market is estimated to be around US$19 billion to US$20 billion. Nowadays, an unnoticed category like smoking cessation stickers is larger than the entire e-cigarette market. Compared with the traditional cigarette market, the e-cigarette market only accounts for less than 2% of the proportion. At present, the profits from burning tobacco are showing a downward trend. The number of smokers around the world is declining. Only China is unique in the number of smokers increasing. As the post-80s and post-90s generation become the main consumers, their demand for burning cigarettes has naturally declined. This is a trend around the world.

Based on the current growth rate of 17%, it can be estimated that by 2030, combustible nicotine products and non-combustible nicotine products will each account for half of the market. Europe is the second largest e-cigarette consumer market outside the United States. Four countries, Britain, Italy, France and Germany, account for more than 90% of the European market. The European market started two to three years later than the American market, but the market growth rate is relatively fast. In China's sales of e-cigarettes in 2015 were 2.7 billion yuan, and in 2016 it was about 3 to 3.2 billion yuan. Online was the main focus and offline was supplemented. The cumulative sales of a single brand on Tmall or Jingdong could reach 100 million yuan. Even if it is a very large brand, there are about 1500 offline stores across the country, and about 10% to 20% of offline stores are profitable. In 2016, the figure for tobacco profits and taxes announced by China Tobacco Monopoly Administration was 1 trillion yuan, and the military expenditure budget for the same year was more than 900 billion yuan. It is estimated that China's e-cigarette market will reach 7.2 billion yuan by 2020. The volume of China's e-cigarette market is very small compared to the above figure. The main reason is that China's policies are unclear. China's e-cigarette market is still in a situation where there is no competent department, no sales regulations, and no market access system. After a series of surveys, it was found that less than 5% of the people in China know about or use e-cigarettes, and this figure in the United States can reach 70%-80%. In summary, the proportion of atomization equipment in the traditional tobacco market is very low, and there is still a lot of room for growth. The current global market growth rate is slowing down compared with the beginning of development.

5. The concentration of e-cigarette market will increase

Many companies making APV products have transformed from their original OEM business. OEM sales brands have become increasingly concentrated. There were about 30 brands in the market, but now they are gradually concentrated to about 10 brands. The concentration of these 10 brands in the domestic supply chain is also gradually increasing, and most manufacturers have been squeezed out. If there is a breakthrough in e-cigarette manufacturing technology, automatic production can be fully realized, and the product model is very single and large, the OEM enterprises may migrate from the current China to the United States. In the future, the equipment market may only be left with several major domestic e-cigarette companies such as Zhuoyue, McWeir, Arips, Kaner, and Xinyikang, and the tobacco oil market will also be concentrated in the hands of several large tobacco oil manufacturers.

6. Risks in the e-cigarette industry

There are risks such as technical trends and exchange rate factors in the e-cigarette industry, but the most critical thing is policy risks. At present, China's e-cigarette market has not entered the stage of standardized operation, and there are no clear regulatory regulations to refer to. Only in the European and American markets, e-cigarettes belong to the system of smoke-like products, and are managed uniformly by the Food and Drug Administration like tobacco, drugs, and medical device products. The EU focuses more on promoting medical certification of e-cigarette products, with more emphasis on clinical and behavioral experiments. After products pass certification, they can be sold in pharmacies. Some countries and regions have ordered bans on the sale and use of electronic nebulized products containing nicotine, such as Australia and Hong Kong. The markets of large e-cigarette companies in Shenzhen are mainly in Europe and the United States, and sales in the European and American markets account for more than 50%. Therefore, domestic companies can only passively adapt to the adjustments and changes in the foreign e-cigarette regulatory system.# p #pagination title #e #

On August 8, 2016, the U.S. Food and Drug Administration (FDA) officially issued a pre-marketing application (PMTA) for tobacco products. Companies that want to continue to engage in e-cigarette sales in the United States must urgently submit application documents within the two-year application period. The FDA will inform the company whether it has passed the review in the third year. The fee for applying for certification for a single product sales category is about US$8 million. The cumulative fee for subsequent products is low, but the main fee is higher. The fee is mainly collected by third-party laboratories and law firms. The implementation of this policy is very likely It was promoted by large tobacco companies through lobbying the government. The introduction of PMAT will enable the FDA to control the e-cigarette market and promote the demonstration of e-cigarettes in terms of safety, material safety and toxicological harmlessness. At present, the EU has not introduced such strict policies as the U.S. market. However, in the future, the EU, including China's e-cigarette market legislation, will use PMTA as a benchmark, and corresponding policies are expected to be introduced in the next two to three years. There will be a closed trend for PMTA certification. E-cigarette equipment needs to be bound tested on specific smoking fluids. After the package certification is passed, it can be bound and sold in the U.S. market. It is expected that the total number of APV companies in the world that will eventually pass PMTA certification should not exceed 30, and corporate products that have not passed the certification will not be able to continue to be sold in the U.S. market.

7. Safety mechanism of electronic cigarettes

The substance that is most harmful to the human body in traditional burning cigarettes is tobacco tar. Nicotine is only addictive at controllable concentrations, but it is harmless to the human body. E-cigarettes can achieve control over nicotine intake. They can not add it, or they can choose different nicotine intake concentrations of high, medium and low according to their own needs. The company will conduct some clinical experiments on nicotine intake satisfaction to explore what nicotine content indicators e-cigarette users can achieve maximum smoking satisfaction.

8. Investment in e-cigarette capital market

Listed companies investing in the e-cigarette market from 2013 to 2014 include Huizhou Yiwei, Jinjia, Luxin, Dongfeng, and Irepus, a well-known e-cigarette company before the Third Board. Hong Kong stock company China Flavors and Fragrances acquired ODM manufacturer Geirui in 15 years and began to deploy in the domestic e-cigarette market. There are many cases abroad. The first case of a large tobacco company acquiring an independent e-cigarette brand occurred in 2012, namely Lorillard's acquisition of BLU ECIGS. The current market share of the BLU e-cigarette brand can probably rank third or fourth. In April 2015, Japan Tobacco International acquired the e-cigarette brand LOGIC. Later, Hong Kong-listed company Warburg acquired VMR Products, and acquisitions occur almost every year.

9. Comparison of heated non-burning cigarettes and e-cigarettes

The tobacco leaf used to heat and unburn tobacco is still traditional tobacco. Tobacco sheet technology is used to directly put the tobacco into the heater, and the tobacco is cured through heating equipment to form smoke for smoking. The amount of smoke is small and the intake of nicotine is also relatively small. The design purpose is to reduce the harm caused by tobacco tar in burning cigarettes to the human body. E-cigarette products are about 10% harmful to the human body, and the harm caused by heating and burning tobacco is about 20% to 30%. This product can be used in an indoor environment, similar to the iPad and the charging treasure, and can be used repeatedly after charging. The Tobacco Monopoly Administration of China does not allow non-tobacco companies to sell, export or import tobacco products. Companies with such products can only make electronic equipment, such as heaters and batteries. At present, the development of heated non-burning tobacco is extremely rapid and is the core focus of traditional tobacco giants. In just 16 years, shipments have reached 30 million, achieving sales of more than 700 million US dollars. IQOS is expected to attract 20% of traditional cigarette users.

Japan Tobacco International's heated non-burn cigarette brand is called Ploom Tech. IQOS is a heated non-burn tobacco owned by Marlboro. IQOS accounts for 70% of the market in Japan. Japan Tobacco International is very dissatisfied with this. It believes that this year's Ploom Tech market share can be equal to IQOS. E-cigarette technology is equivalent to pure electric vehicles. After all, the physical principles of solid atomization and solid combustion are different. At present, due to imperfect technology, it cannot fully meet users 'needs, such as taste, which has resulted in the birth of a hybrid product of heating and non-burning tobacco. This product is closer to traditional tobacco and is more harmful to the human body than e-cigarettes, but it can get closer to traditional smokers and be more attractive to consumers of traditional cigarettes. With the update and iteration of e-cigarette technology, user satisfaction continues to increase. When the experience between e-cigarettes and real cigarettes is close to more than 95%, a series of technologies such as taste, concentration, cost performance, and harmlessness to human bodies are simultaneously solved. Problems, the business of heating tobacco without burning will disappear. At the same time, there are also views that the rapid development of heated non-burning cigarettes may also suppress the e-cigarette market.# p#pagination title #e#

The overall consumer group is divided into two categories. APV consumers are relatively young. They are not smokers. Out of a show-off mentality, they are attracted by the fashionable shape design and large smoke volume of APV e-cigarettes, meeting the needs of communication and social networking. Influenced by hippie culture, American middle school students mainly use e-cigarette products. Consumers who heat non-burn tobacco are themselves smokers. As a substitute for traditional cigarettes, with IQOS's continuous investment in product shape research and development and design, heating non-burn tobacco has also become a trend. The use of e-cigarettes mainly has three needs: quitting smoking, replacing cigarettes and pursuing a fashionable lifestyle. The potential market demand for quitting smoking and replacing cigarettes should be greater. Living needs pursue large quantities of tobacco. We can estimate the lifestyle market by using the total shipments of DNA and Yihai chips minus the number of dense equipment. Sales of nicotine-free tobacco oil account for more than 50% of the total tobacco oil sales. proportion. 10. Consumables of e-cigarettes

10. Consumables of e-cigarettes

The main consumables in e-cigarettes are atomizing cores and tobacco oil. The atomizing cores need to be replaced every one to two weeks. A 5ml bottle of tobacco oil can be used for about a week, and the price is about 5 US dollars. Equipment has a great impact on the taste of e-cigarettes. Equipment and tobacco and tobacco oil brands are not mixed together, but are sold separately.

11. Differences between companies and large tobacco companies

The company's capabilities lie in electronic equipment, such as batteries, atomizers, chips, heaters, etc. The capabilities of large tobacco companies are concentrated on the research and development of tobacco-related products, such as tobacco sheet technology, tobacco oil blending technology, flavors and fragrances. Safety technology and research and development technology for multiple flavors of tobacco oil and tobacco. In the United States, there are 10 large tobacco companies that have the ability to produce tobacco. The technical threshold for tobacco oil blending is low. As long as the safety of raw materials is ensured, there are thousands of companies that have the ability to produce tobacco oil. There are no e-cigarette equipment manufacturers in the United States. The supply chain of these equipment is all in China. China's equipment exports account for one-fifth of the U.S. market. About 200 domestic companies have exported equipment, and McQuell accounts for about 20% of the export market share.

12. E-cigarette sales channels

Channel operations mainly include two dimensions: distribution and after-sales. Product distribution is done by secondary channels. Currently, the company has nearly 130 dealers in the United States. Product sales are not as complicated as imagined. The company itself does not have many e-cigarette categories, and will not directly deliver goods to retail investors. The sales front will not be long, and there is not much pressure to shop goods. Thirty to fifty sets of goods can be sold out quickly, which reflects the value of the dealer. The company does not set standards for the decoration and brand management in dealer stores. It is impossible for dealers to sell only a certain brand of e-cigarette products. The best-selling products will be placed in a conspicuous position in the store.

13. E-cigarette hits occur

E-cigarette products have a pyramid structure of entry-level, gamer level, and enthusiast level. The first-mover advantage and market positioning of the product are relatively important. Last year, the hit model made by Arips was mainly aimed at e-cigarette enthusiasts. The product uses a dual heating wire architecture and belongs to the top-level equipment. It is hard to imagine that this product can sold well in such a niche market, with sales reaching 1 billion RMB. Technical attributes are also a very important factor. The taste, purity and smoke volume of the smoke will affect product sales. A product with monthly sales volume of 1 million units can be called a hit. The iteration speed of an e-cigarette category is less than 18 months, and the entire industry is undergoing rapid updates. Currently, the company's products are only targeted at the entry-level market.

The company's current business includes two major sectors: ODM and private brand APV. The company has core patented technologies for e-cigarettes such as ceramic heaters and child protection. The core team has many years of professional operation experience in R & D, manufacturing, and customer channels in the e-cigarette industry, and provides application of company patents to large overseas tobacco companies Altria, Japan Tobacco International, etc. Technology e-cigarette products. APV's own brand Vaporesso series products of the Open Electronic Atomization Equipment Division have formed a certain market scale and end customer influence in overseas markets.

The company has long-term accumulation in various aspects such as process technology, product quality, and R & D strength. The company forms the main source of income through ODM order sales and the distribution model of overseas APV atomization equipment specialty stores. During the reporting period, while ODM business increased steadily, APV business formed a stable source of income, accounting for about 30% of overall operating income.

1. company's development history

McWare Co., Ltd. was established in 2009. At the end of October and the beginning of November, the first disposable e-cigarette product reached large-scale sales. In 2012, shipments of upgraded products could reach 2 million to 3 million a month. The company's products are in the United States The market has begun to enter a rapid development cycle. In 2013, driven by customers, sales terminals in the U.S. market were established, mainly involving major pharmacies in the United States and large supermarkets such as Wal-Mart, raising the entry barrier for the industry. In 2014, it carried out capital integration with listed company Huizhou Yiwei and acquired part of the company's equity. In 2015, it obtained the national high-tech certification and was officially listed on the New Third Board. In 2016, six market-making brokerages were introduced in two rounds. In the same year, the company's technical team was established and the industry's first dust-free workshop was established. The company has a long working time and rich experience, which has promoted the establishment of industry manufacturing standards. It also helped Shenzhen Customs formulate e-cigarette export codes, making certain contributions to the development of the e-cigarette market.

2. The company's traditional ODM business and emerging APV business are driven by dual enginesThe company mainly involves two parts of business, one of which is ODM business. The brand of this business belongs to customers. The company provides ODM OEM manufacturing services. The customer service is responsible for controlling the marketing, marketing, branding and distribution. Such products are mainly sold in traditional cigarette market channels, such as gas stations, convenience stores and tobacco monopoly counters in large supermarkets. They are used as a substitute for smokers to burn cigarettes in smoke-free occasions. There is no cigarette equipment in the ODM business. The other is APV's private brand business. Currently, the company has three major brands, which mainly rely on offline experience stores for sales. Traditional tobacco is like beer. To buy beer, you need to go to a supermarket. E-cigarettes are like red wine. To buy red wine, you need to go to a wine specialty store. You can get some experience and communication. The cigarette and e-cigarette markets will not overlap in the foreseeable future. In all e-cigarette offline experience stores in the United States, all APV equipment is produced by China manufacturers, but cigarette oil manufacturers are both from the United States and China.

The customers of the company's ODM business are mainly large global tobacco companies, such as Altria (Marlboro), Japan Tobacco International, British American Tobacco (35 brand cigarettes), Luxembourg, and Swedish Match. Before 2010, large tobacco companies did not intervene in the e-cigarette business, and successively entered the e-cigarette market through mergers and acquisitions of independent e-cigarette brands. For ODM business, the company only needs to do a good job in process control and quality control to meet customers 'shipment point requirements. For self-owned APV brands, in addition to products, we must also consider the issues of brand management and channel sales. In terms of private brand building, Youtube, Facebook, TWITTER and other media are used to do self-media marketing. Youtube had more than 45000 videos to promote its own brand last year, and its official website also exceeded 11 million visitors. In 2017, its own products covered 38 countries and had more than 130 agencies around the world. Overall, the company's business growth rate in the past 17 years should reach 30%. Driven by the dual engines of traditional ODM business and emerging APV business, these two aspects of business will be flat in the future.# p#pagination title #e#

3. The core technology of e-cigarettes

The four core technologies of e-cigarettes are batteries, tobacco oil, atomizer (ic), and heaters. Now, profit-making sales are the two products produced by APV and ODM. Currently, heating and non-burning tobacco is very popular on the market (accounting for 7% of Japan's traditional cigarette market, and it is expected to reach 20% this year) adopts the common platform technology of e-cigarettes, such as core heater materials, atomization technology, batteries, etc. E-cigarette technology has great extensibility. For example, medical drug delivery technology uses an electronic heater to heat a coated solid drug. The drug sublimates into a gas and is directly absorbed through the mouth. Another example is the electronic use of hookah, which does not require carbon heating. Electronic ceramic pots are used to heat hookah. Currently, such products have not yet been sold on a large scale.

4. The e-cigarette market has great room for growth

In 2016, the global market share of e-cigarettes was about US$20 billion, and the United States accounted for about 50% of the market. The United States formed large-scale sales in about 2010, which is basically the same as the time when the company formed large-scale sales. The company caught up with the U.S. market. The first step to take off. At present, the growth rate of the e-cigarette market is slowing down, not as fast as in the first five years. In recent years, the market growth rate has remained at around 17%. By 2020, the e-cigarette market is estimated to be around US$19 billion to US$20 billion. Nowadays, an unnoticed category like smoking cessation stickers is larger than the entire e-cigarette market. Compared with the traditional cigarette market, the e-cigarette market only accounts for less than 2% of the proportion. At present, the profits from burning tobacco are showing a downward trend. The number of smokers around the world is declining. Only China is unique in the number of smokers increasing. As the post-80s and post-90s generation become the main consumers, their demand for burning cigarettes has naturally declined. This is a trend around the world.

Based on the current growth rate of 17%, it can be estimated that by 2030, combustible nicotine products and non-combustible nicotine products will each account for half of the market. Europe is the second largest e-cigarette consumer market outside the United States. Four countries, Britain, Italy, France and Germany, account for more than 90% of the European market. The European market started two to three years later than the American market, but the market growth rate is relatively fast. In China's sales of e-cigarettes in 2015 were 2.7 billion yuan, and in 2016 it was about 3 to 3.2 billion yuan. Online was the main focus and offline was supplemented. The cumulative sales of a single brand on Tmall or Jingdong could reach 100 million yuan. Even if it is a very large brand, there are about 1500 offline stores across the country, and about 10% to 20% of offline stores are profitable. In 2016, the figure for tobacco profits and taxes announced by China Tobacco Monopoly Administration was 1 trillion yuan, and the military expenditure budget for the same year was more than 900 billion yuan. It is estimated that China's e-cigarette market will reach 7.2 billion yuan by 2020. The volume of China's e-cigarette market is very small compared to the above figure. The main reason is that China's policies are unclear. China's e-cigarette market is still in a situation where there is no competent department, no sales regulations, and no market access system. After a series of surveys, it was found that less than 5% of the people in China know about or use e-cigarettes, and this figure in the United States can reach 70%-80%. In summary, the proportion of atomization equipment in the traditional tobacco market is very low, and there is still a lot of room for growth. The current global market growth rate is slowing down compared with the beginning of development.

5. The concentration of e-cigarette market will increase

Many companies making APV products have transformed from their original OEM business. OEM sales brands have become increasingly concentrated. There were about 30 brands in the market, but now they are gradually concentrated to about 10 brands. The concentration of these 10 brands in the domestic supply chain is also gradually increasing, and most manufacturers have been squeezed out. If there is a breakthrough in e-cigarette manufacturing technology, automatic production can be fully realized, and the product model is very single and large, the OEM enterprises may migrate from the current China to the United States. In the future, the equipment market may only be left with several major domestic e-cigarette companies such as Zhuoyue, McWeir, Arips, Kaner, and Xinyikang, and the tobacco oil market will also be concentrated in the hands of several large tobacco oil manufacturers.

6. Risks in the e-cigarette industry

There are risks such as technical trends and exchange rate factors in the e-cigarette industry, but the most critical thing is policy risks. At present, China's e-cigarette market has not entered the stage of standardized operation, and there are no clear regulatory regulations to refer to. Only in the European and American markets, e-cigarettes belong to the system of smoke-like products, and are managed uniformly by the Food and Drug Administration like tobacco, drugs, and medical device products. The EU focuses more on promoting medical certification of e-cigarette products, with more emphasis on clinical and behavioral experiments. After products pass certification, they can be sold in pharmacies. Some countries and regions have ordered bans on the sale and use of electronic nebulized products containing nicotine, such as Australia and Hong Kong. The markets of large e-cigarette companies in Shenzhen are mainly in Europe and the United States, and sales in the European and American markets account for more than 50%. Therefore, domestic companies can only passively adapt to the adjustments and changes in the foreign e-cigarette regulatory system.# p #pagination title #e #

On August 8, 2016, the U.S. Food and Drug Administration (FDA) officially issued a pre-marketing application (PMTA) for tobacco products. Companies that want to continue to engage in e-cigarette sales in the United States must urgently submit application documents within the two-year application period. The FDA will inform the company whether it has passed the review in the third year. The fee for applying for certification for a single product sales category is about US$8 million. The cumulative fee for subsequent products is low, but the main fee is higher. The fee is mainly collected by third-party laboratories and law firms. The implementation of this policy is very likely It was promoted by large tobacco companies through lobbying the government. The introduction of PMAT will enable the FDA to control the e-cigarette market and promote the demonstration of e-cigarettes in terms of safety, material safety and toxicological harmlessness. At present, the EU has not introduced such strict policies as the U.S. market. However, in the future, the EU, including China's e-cigarette market legislation, will use PMTA as a benchmark, and corresponding policies are expected to be introduced in the next two to three years. There will be a closed trend for PMTA certification. E-cigarette equipment needs to be bound tested on specific smoking fluids. After the package certification is passed, it can be bound and sold in the U.S. market. It is expected that the total number of APV companies in the world that will eventually pass PMTA certification should not exceed 30, and corporate products that have not passed the certification will not be able to continue to be sold in the U.S. market.

7. Safety mechanism of electronic cigarettes

The substance that is most harmful to the human body in traditional burning cigarettes is tobacco tar. Nicotine is only addictive at controllable concentrations, but it is harmless to the human body. E-cigarettes can achieve control over nicotine intake. They can not add it, or they can choose different nicotine intake concentrations of high, medium and low according to their own needs. The company will conduct some clinical experiments on nicotine intake satisfaction to explore what nicotine content indicators e-cigarette users can achieve maximum smoking satisfaction.

8. Investment in e-cigarette capital market

Listed companies investing in the e-cigarette market from 2013 to 2014 include Huizhou Yiwei, Jinjia, Luxin, Dongfeng, and Irepus, a well-known e-cigarette company before the Third Board. Hong Kong stock company China Flavors and Fragrances acquired ODM manufacturer Geirui in 15 years and began to deploy in the domestic e-cigarette market. There are many cases abroad. The first case of a large tobacco company acquiring an independent e-cigarette brand occurred in 2012, namely Lorillard's acquisition of BLU ECIGS. The current market share of the BLU e-cigarette brand can probably rank third or fourth. In April 2015, Japan Tobacco International acquired the e-cigarette brand LOGIC. Later, Hong Kong-listed company Warburg acquired VMR Products, and acquisitions occur almost every year.

9. Comparison of heated non-burning cigarettes and e-cigarettes

The tobacco leaf used to heat and unburn tobacco is still traditional tobacco. Tobacco sheet technology is used to directly put the tobacco into the heater, and the tobacco is cured through heating equipment to form smoke for smoking. The amount of smoke is small and the intake of nicotine is also relatively small. The design purpose is to reduce the harm caused by tobacco tar in burning cigarettes to the human body. E-cigarette products are about 10% harmful to the human body, and the harm caused by heating and burning tobacco is about 20% to 30%. This product can be used in an indoor environment, similar to the iPad and the charging treasure, and can be used repeatedly after charging. The Tobacco Monopoly Administration of China does not allow non-tobacco companies to sell, export or import tobacco products. Companies with such products can only make electronic equipment, such as heaters and batteries. At present, the development of heated non-burning tobacco is extremely rapid and is the core focus of traditional tobacco giants. In just 16 years, shipments have reached 30 million, achieving sales of more than 700 million US dollars. IQOS is expected to attract 20% of traditional cigarette users.

Japan Tobacco International's heated non-burn cigarette brand is called Ploom Tech. IQOS is a heated non-burn tobacco owned by Marlboro. IQOS accounts for 70% of the market in Japan. Japan Tobacco International is very dissatisfied with this. It believes that this year's Ploom Tech market share can be equal to IQOS. E-cigarette technology is equivalent to pure electric vehicles. After all, the physical principles of solid atomization and solid combustion are different. At present, due to imperfect technology, it cannot fully meet users 'needs, such as taste, which has resulted in the birth of a hybrid product of heating and non-burning tobacco. This product is closer to traditional tobacco and is more harmful to the human body than e-cigarettes, but it can get closer to traditional smokers and be more attractive to consumers of traditional cigarettes. With the update and iteration of e-cigarette technology, user satisfaction continues to increase. When the experience between e-cigarettes and real cigarettes is close to more than 95%, a series of technologies such as taste, concentration, cost performance, and harmlessness to human bodies are simultaneously solved. Problems, the business of heating tobacco without burning will disappear. At the same time, there are also views that the rapid development of heated non-burning cigarettes may also suppress the e-cigarette market.# p#pagination title #e#

The overall consumer group is divided into two categories. APV consumers are relatively young. They are not smokers. Out of a show-off mentality, they are attracted by the fashionable shape design and large smoke volume of APV e-cigarettes, meeting the needs of communication and social networking. Influenced by hippie culture, American middle school students mainly use e-cigarette products. Consumers who heat non-burn tobacco are themselves smokers. As a substitute for traditional cigarettes, with IQOS's continuous investment in product shape research and development and design, heating non-burn tobacco has also become a trend. The use of e-cigarettes mainly has three needs: quitting smoking, replacing cigarettes and pursuing a fashionable lifestyle. The potential market demand for quitting smoking and replacing cigarettes should be greater. Living needs pursue large quantities of tobacco. We can estimate the lifestyle market by using the total shipments of DNA and Yihai chips minus the number of dense equipment. Sales of nicotine-free tobacco oil account for more than 50% of the total tobacco oil sales. proportion.

10. Consumables of e-cigarettesThe main consumables in e-cigarettes are atomizing cores and tobacco oil. The atomizing cores need to be replaced every one to two weeks. A 5ml bottle of tobacco oil can be used for about a week, and the price is about 5 US dollars. Equipment has a great impact on the taste of e-cigarettes. Equipment and tobacco and tobacco oil brands are not mixed together, but are sold separately.

11. Differences between companies and large tobacco companies

The company's capabilities lie in electronic equipment, such as batteries, atomizers, chips, heaters, etc. The capabilities of large tobacco companies are concentrated on the research and development of tobacco-related products, such as tobacco sheet technology, tobacco oil blending technology, flavors and fragrances. Safety technology and research and development technology for multiple flavors of tobacco oil and tobacco. In the United States, there are 10 large tobacco companies that have the ability to produce tobacco. The technical threshold for tobacco oil blending is low. As long as the safety of raw materials is ensured, there are thousands of companies that have the ability to produce tobacco oil. There are no e-cigarette equipment manufacturers in the United States. The supply chain of these equipment is all in China. China's equipment exports account for one-fifth of the U.S. market. About 200 domestic companies have exported equipment, and McQuell accounts for about 20% of the export market share.

12. E-cigarette sales channels

Channel operations mainly include two dimensions: distribution and after-sales. Product distribution is done by secondary channels. Currently, the company has nearly 130 dealers in the United States. Product sales are not as complicated as imagined. The company itself does not have many e-cigarette categories, and will not directly deliver goods to retail investors. The sales front will not be long, and there is not much pressure to shop goods. Thirty to fifty sets of goods can be sold out quickly, which reflects the value of the dealer. The company does not set standards for the decoration and brand management in dealer stores. It is impossible for dealers to sell only a certain brand of e-cigarette products. The best-selling products will be placed in a conspicuous position in the store.

13. E-cigarette hits occur

E-cigarette products have a pyramid structure of entry-level, gamer level, and enthusiast level. The first-mover advantage and market positioning of the product are relatively important. Last year, the hit model made by Arips was mainly aimed at e-cigarette enthusiasts. The product uses a dual heating wire architecture and belongs to the top-level equipment. It is hard to imagine that this product can sold well in such a niche market, with sales reaching 1 billion RMB. Technical attributes are also a very important factor. The taste, purity and smoke volume of the smoke will affect product sales. A product with monthly sales volume of 1 million units can be called a hit. The iteration speed of an e-cigarette category is less than 18 months, and the entire industry is undergoing rapid updates. Currently, the company's products are only targeted at the entry-level market.