2018 E-Cigarette Industry Analysis Report

2018 E-cigarette Industry Analysis Report: The e-cigarette industry has been a mature sector overseas for nearly a decade. In the United States and Europe alone, it has produced companies such as Philip Morris International, whose IQOS products generated

2018 E-Cigarette Industry Analysis Report: The e-cigarette industry has developed into a mature sector overseas for nearly a decade. In the U.S. and European markets, companies like Philip Morris International (with IQOS products generating 36 billion yuan in 2017) and JUUL (valued at nearly $20 billion) have emerged. In the global e-cigarette market, the U.S. holds a 50% market share, while China, which accounts for over a quarter of global traditional cigarette sales, has an e-cigarette market share of less than 1%. However, the Shenzhen area contributes over 95% of global e-cigarette OEM production capacity.

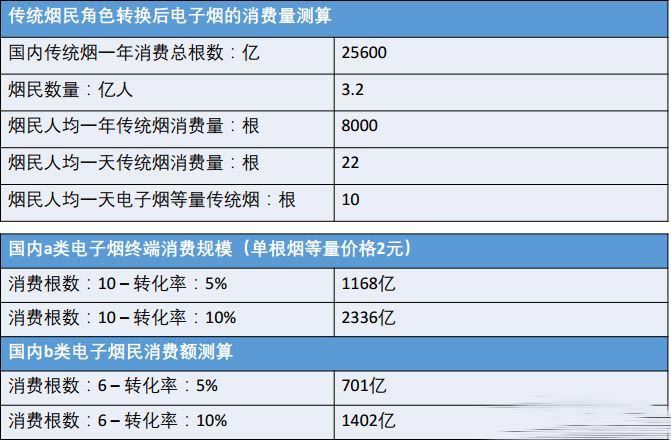

According to Research and Markets, global e-cigarette sales reached $7 billion in 2016, maintaining a year-on-year growth rate of over 25% for nearly five years. The Chinese market is roughly estimated to have sales of less than 1 billion yuan in 2017, with the overall market size exceeding 100 billion yuan based on the conversion rate of traditional smokers.

This article briefly discusses the e-cigarette industry from three aspects: basic classification & principles, market conditions, and some viewpoints.

1. Basic Classification & Principles of E-Cigarettes

Currently, there are three main types of e-cigarettes: 1: HNB (Heat Not Burn), represented by IQOS, which heats tobacco at a high temperature of 300°C without combustion; 2: Oil-filled atomizers, represented by SMOK, which inject e-liquid to produce a large amount of vapor; 3: Pod systems, represented by JUUL, which use nicotine pods to create a sensation similar to traditional cigarettes.

1. HNB

The basic principle of HNB products is to heat tobacco to produce nicotine intake, which closely resembles the experience of smoking a lit cigarette. In terms of health, the absence of combustion significantly reduces tar production and eliminates hundreds of unknown harmful substances generated during the burning process.

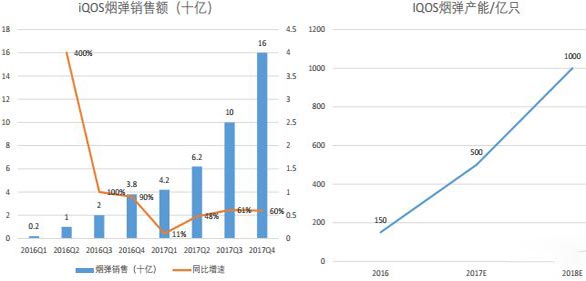

The representative product, IQOS, is the core product of Philip Morris International (Marlboro). Its market share in the U.S., Europe, Japan, and South Korea has rapidly increased, achieving nearly 20% market share in mature markets. It is reported that Philip Morris International considers this as a core strategy to replace Marlboro. The IQOS system includes HNB devices and specially designed tobacco sticks, with many manufacturers producing devices in the Chinese market. The core technology focuses on the stability and continuity of the heating element and the thermal insulation of the casing. The tobacco sticks are processed through special techniques and are regulated under traditional cigarette sales and production regulations. Traditional tobacco sticks are generally supplied by Marlboro, while domestic brands like Kuan Zhai Xiang Zi are also actively developing such products.

There are also HNB products from Brand A that directly heat traditional tobacco (like Yuxi), but these products currently struggle to replicate the flavors of different traditional tobacco brands.

IQOS is priced at over 1000 yuan, while domestic devices are around 600 yuan.

IQOS is priced at over 1000 yuan, while domestic devices are around 600 yuan.

2. Oil-filled Atomizers (the following refers to oil-filled and pod nicotine as added nicotine salts.)

Generally considered as "player" products, they inject e-liquid into the device, generating a large amount of vapor with high power. The e-liquid typically contains little to no nicotine (in very small amounts) and offers a variety of flavors (tobacco, fruit, coffee, beverages, etc.). The representative company is IVPS (SMOK, listed on the New Third Board).

Large vapor devices generally range from 150 to 400 yuan, with e-liquid priced between 50 to 150 yuan for 100ml. Different brands of e-liquid are generally compatible with various brands of devices, lacking exclusivity.

Due to the negligible smoking cessation or quitting effects of large vapor devices, this section will not be elaborated on.

3. Pod Systems (Rechargeable E-Cigarettes with Replaceable Pods)

Rechargeable devices that use replaceable pods containing nicotine e-liquid (generally between 2%-6% nicotine concentration) provide a throat hit and vaporization effect similar to traditional cigarettes, making them a primary choice for smoking cessation and new smokers. These products only provide nicotine intake without producing tar or other harmful substances, making them the healthiest option for nicotine consumption currently available.

The pods are disposable products sold directly by manufacturers, and users cannot refill them. Each pod can provide between 300 to 500 puffs, equivalent to a pack of cigarettes.

The representative company, JUUL, received a $650 million investment from Tiger in 2018, with a valuation exceeding $15 billion. It occupies 70% of the U.S. e-cigarette market, with sales doubling quarter over quarter in the past three years. #p#分页标题#e#

Due to the rapid popularity of its products and incomplete regulatory policies, the U.S. FDA is increasingly monitoring its sales to minors.

Pod devices generally range from 200 to 400 yuan, with individual pods priced between 25 to 50 yuan. Generally, specific brand pods are only compatible with specific brand devices.

The market also includes disposable pod systems and non-rechargeable, single-use types, which contain about 300 puffs of e-liquid and are generally priced between 30 to 50 yuan. Their flavor restoration and product positioning are weaker compared to rechargeable pod systems, so they will not be discussed in depth.

2. Basic Overview of the Pod Market

The pod industry chain can be roughly divided into: 1: Upstream - device manufacturers (OEM) and e-liquid producers; 2: Brands; 3: Downstream sales. As an experienced user and observer of e-cigarettes, this article will only provide a general analysis of the pod market without going into specifics.

1. Upstream - Device Manufacturers

Device manufacturers have three characteristics: mature enterprises, labor-intensive, and relatively limited technological competition.

Device manufacturers (OEM) generally produce oil-filled atomizers and pod systems for overseas markets, including more than five listed companies such as IVPS, Macwell, and Sigelei. Different manufacturers compete fiercely in the production process of e-cigarettes, with the core components being the structure, battery, and atomizer (pod). The main competitive barrier lies in the atomizer.

The atomizer (pod) directly determines the vaporization effect, flavor, and throat hit of the e-liquid. Currently, mainstream atomizer cores include cotton and ceramic heating elements, with ceramic cores being more commonly used in recent years (to avoid burning cotton).

In the current early market stage, most pod users are first-time e-cigarette users, with aesthetics and compatibility with traditional cigarettes being the primary considerations. As market awareness rapidly advances, users will compare different brands of e-cigarettes, and technological competition in atomizers will become the core focus for manufacturers vying for the e-cigarette market.

2. Upstream - E-Liquid

E-liquid manufacturers are relatively concentrated, with high technical barriers, mainly focusing on the restoration of traditional cigarette flavors after adding different nicotine salts. Additionally, different product categories are similar to wine, with specialized flavorists adjusting different flavors for various pod devices, resulting in significant flavor differences among the same flavor from different brands.

Currently, pod e-liquid flavors include mainstream tobacco, mint, various fruits, as well as unique flavors like beverages, alcohol, and tea.

4. Brands

In the early market stage, there are significant opportunities for brand building and market capture, with considerable expected growth potential. 2018 marked the original year for pod systems in China, following the awareness cultivated by products like IQOS and SMOK, and the consumption upgrade promoting users' attention to health and new products, many brands have experienced market dividends and rapid growth.

In the early market stage, there are significant opportunities for brand building and market capture, with considerable expected growth potential. 2018 marked the original year for pod systems in China, following the awareness cultivated by products like IQOS and SMOK, and the consumption upgrade promoting users' attention to health and new products, many brands have experienced market dividends and rapid growth.

Currently, mainstream pod brands in China include international brands like JUUL, as well as domestic brands R, N, P, S, M, etc. Leading brands can achieve over 50% month-on-month growth, with monthly sales of over a million pods. Among these brands, the positioning, structural design, and flavor differences are quite distinct.

Generally, more advantageous brands have upstream OEM manufacturers maintaining exclusivity over their products. Additionally, due to the strict compatibility between pods and devices, users face high switching costs, and the usage scenarios and habits of e-cigarettes are superior to traditional cigarettes, leading to higher user loyalty.

4. Sales

Currently, the domestic e-cigarette market is still in its early stages, with a significant portion of sales coming from overseas distribution and domestic distributors accumulated from oil-filled e-cigarettes and HNB products, while new brands are beginning to build their own online sales channels, and some brands are actively promoting offline channels.

Due to the sensitivity of the products, although there are currently no explicit regulatory restrictions, and e-cigarettes are classified as online products, the high user loyalty and sensitive policy restrictions make selecting stable and rapid user acquisition channels key to brand competition.

3. Some Viewpoints

1. The e-cigarette industry in China is a typical emerging market, with a dispersed and low brand share, and a broad expected market space. It is hoped that it will gradually develop under reasonable regulation and give rise to strong brands.

2. Tobacco tax revenue is an important source of tax revenue in various countries, and regulation of its layout is a significant focus. Currently, domestic regulation mainly targets HNB tobacco (due to its special processing as traditional tobacco), but as development progresses, regulations on oil-filled tobacco and pod systems will gradually improve, with active cooperation in the regulatory process and protection of minors being a priority during industry development. #p#分页标题#e#

3. The technological barriers of upstream manufacturers in the e-cigarette industry chain evolve and protect relatively slowly, while the compatibility and specificity between devices and e-liquids are high. Therefore, the technical differences among different brands are minimal, focusing instead on flavor, structure, and market positioning, while channel construction remains incomplete. It is hoped that enterprises will emerge from this vast market.

According to Research and Markets, global e-cigarette sales reached $7 billion in 2016, maintaining a year-on-year growth rate of over 25% for nearly five years. The Chinese market is roughly estimated to have sales of less than 1 billion yuan in 2017, with the overall market size exceeding 100 billion yuan based on the conversion rate of traditional smokers.

This article briefly discusses the e-cigarette industry from three aspects: basic classification & principles, market conditions, and some viewpoints.

1. Basic Classification & Principles of E-Cigarettes

Currently, there are three main types of e-cigarettes: 1: HNB (Heat Not Burn), represented by IQOS, which heats tobacco at a high temperature of 300°C without combustion; 2: Oil-filled atomizers, represented by SMOK, which inject e-liquid to produce a large amount of vapor; 3: Pod systems, represented by JUUL, which use nicotine pods to create a sensation similar to traditional cigarettes.

1. HNB

The basic principle of HNB products is to heat tobacco to produce nicotine intake, which closely resembles the experience of smoking a lit cigarette. In terms of health, the absence of combustion significantly reduces tar production and eliminates hundreds of unknown harmful substances generated during the burning process.

The representative product, IQOS, is the core product of Philip Morris International (Marlboro). Its market share in the U.S., Europe, Japan, and South Korea has rapidly increased, achieving nearly 20% market share in mature markets. It is reported that Philip Morris International considers this as a core strategy to replace Marlboro. The IQOS system includes HNB devices and specially designed tobacco sticks, with many manufacturers producing devices in the Chinese market. The core technology focuses on the stability and continuity of the heating element and the thermal insulation of the casing. The tobacco sticks are processed through special techniques and are regulated under traditional cigarette sales and production regulations. Traditional tobacco sticks are generally supplied by Marlboro, while domestic brands like Kuan Zhai Xiang Zi are also actively developing such products.

There are also HNB products from Brand A that directly heat traditional tobacco (like Yuxi), but these products currently struggle to replicate the flavors of different traditional tobacco brands.

IQOS is priced at over 1000 yuan, while domestic devices are around 600 yuan.2. Oil-filled Atomizers (the following refers to oil-filled and pod nicotine as added nicotine salts.)

Generally considered as "player" products, they inject e-liquid into the device, generating a large amount of vapor with high power. The e-liquid typically contains little to no nicotine (in very small amounts) and offers a variety of flavors (tobacco, fruit, coffee, beverages, etc.). The representative company is IVPS (SMOK, listed on the New Third Board).

Large vapor devices generally range from 150 to 400 yuan, with e-liquid priced between 50 to 150 yuan for 100ml. Different brands of e-liquid are generally compatible with various brands of devices, lacking exclusivity.

Due to the negligible smoking cessation or quitting effects of large vapor devices, this section will not be elaborated on.

3. Pod Systems (Rechargeable E-Cigarettes with Replaceable Pods)

Rechargeable devices that use replaceable pods containing nicotine e-liquid (generally between 2%-6% nicotine concentration) provide a throat hit and vaporization effect similar to traditional cigarettes, making them a primary choice for smoking cessation and new smokers. These products only provide nicotine intake without producing tar or other harmful substances, making them the healthiest option for nicotine consumption currently available.

The pods are disposable products sold directly by manufacturers, and users cannot refill them. Each pod can provide between 300 to 500 puffs, equivalent to a pack of cigarettes.

The representative company, JUUL, received a $650 million investment from Tiger in 2018, with a valuation exceeding $15 billion. It occupies 70% of the U.S. e-cigarette market, with sales doubling quarter over quarter in the past three years. #p#分页标题#e#

Due to the rapid popularity of its products and incomplete regulatory policies, the U.S. FDA is increasingly monitoring its sales to minors.

Pod devices generally range from 200 to 400 yuan, with individual pods priced between 25 to 50 yuan. Generally, specific brand pods are only compatible with specific brand devices.

The market also includes disposable pod systems and non-rechargeable, single-use types, which contain about 300 puffs of e-liquid and are generally priced between 30 to 50 yuan. Their flavor restoration and product positioning are weaker compared to rechargeable pod systems, so they will not be discussed in depth.

2. Basic Overview of the Pod Market

The pod industry chain can be roughly divided into: 1: Upstream - device manufacturers (OEM) and e-liquid producers; 2: Brands; 3: Downstream sales. As an experienced user and observer of e-cigarettes, this article will only provide a general analysis of the pod market without going into specifics.

1. Upstream - Device Manufacturers

Device manufacturers have three characteristics: mature enterprises, labor-intensive, and relatively limited technological competition.

Device manufacturers (OEM) generally produce oil-filled atomizers and pod systems for overseas markets, including more than five listed companies such as IVPS, Macwell, and Sigelei. Different manufacturers compete fiercely in the production process of e-cigarettes, with the core components being the structure, battery, and atomizer (pod). The main competitive barrier lies in the atomizer.

The atomizer (pod) directly determines the vaporization effect, flavor, and throat hit of the e-liquid. Currently, mainstream atomizer cores include cotton and ceramic heating elements, with ceramic cores being more commonly used in recent years (to avoid burning cotton).

In the current early market stage, most pod users are first-time e-cigarette users, with aesthetics and compatibility with traditional cigarettes being the primary considerations. As market awareness rapidly advances, users will compare different brands of e-cigarettes, and technological competition in atomizers will become the core focus for manufacturers vying for the e-cigarette market.

2. Upstream - E-Liquid

E-liquid manufacturers are relatively concentrated, with high technical barriers, mainly focusing on the restoration of traditional cigarette flavors after adding different nicotine salts. Additionally, different product categories are similar to wine, with specialized flavorists adjusting different flavors for various pod devices, resulting in significant flavor differences among the same flavor from different brands.

Currently, pod e-liquid flavors include mainstream tobacco, mint, various fruits, as well as unique flavors like beverages, alcohol, and tea.

4. Brands

In the early market stage, there are significant opportunities for brand building and market capture, with considerable expected growth potential. 2018 marked the original year for pod systems in China, following the awareness cultivated by products like IQOS and SMOK, and the consumption upgrade promoting users' attention to health and new products, many brands have experienced market dividends and rapid growth.Currently, mainstream pod brands in China include international brands like JUUL, as well as domestic brands R, N, P, S, M, etc. Leading brands can achieve over 50% month-on-month growth, with monthly sales of over a million pods. Among these brands, the positioning, structural design, and flavor differences are quite distinct.

Generally, more advantageous brands have upstream OEM manufacturers maintaining exclusivity over their products. Additionally, due to the strict compatibility between pods and devices, users face high switching costs, and the usage scenarios and habits of e-cigarettes are superior to traditional cigarettes, leading to higher user loyalty.

4. Sales

Currently, the domestic e-cigarette market is still in its early stages, with a significant portion of sales coming from overseas distribution and domestic distributors accumulated from oil-filled e-cigarettes and HNB products, while new brands are beginning to build their own online sales channels, and some brands are actively promoting offline channels.

Due to the sensitivity of the products, although there are currently no explicit regulatory restrictions, and e-cigarettes are classified as online products, the high user loyalty and sensitive policy restrictions make selecting stable and rapid user acquisition channels key to brand competition.

3. Some Viewpoints

1. The e-cigarette industry in China is a typical emerging market, with a dispersed and low brand share, and a broad expected market space. It is hoped that it will gradually develop under reasonable regulation and give rise to strong brands.

2. Tobacco tax revenue is an important source of tax revenue in various countries, and regulation of its layout is a significant focus. Currently, domestic regulation mainly targets HNB tobacco (due to its special processing as traditional tobacco), but as development progresses, regulations on oil-filled tobacco and pod systems will gradually improve, with active cooperation in the regulatory process and protection of minors being a priority during industry development. #p#分页标题#e#

3. The technological barriers of upstream manufacturers in the e-cigarette industry chain evolve and protect relatively slowly, while the compatibility and specificity between devices and e-liquids are high. Therefore, the technical differences among different brands are minimal, focusing instead on flavor, structure, and market positioning, while channel construction remains incomplete. It is hoped that enterprises will emerge from this vast market.